Solutions for Banks

& Digital Transformation

Fintech

The era of API and PSD2

APIs create the conditions for cooperation between traditional banks and technology providers, which results in new services used by digital customers and a transformed business model.

As technology is advancing and more and more users of banking services are adopting the digital operating model, Banks are struggling to provide products, solutions, applications and systems that satisfy digital customers.

Banks, as organizations, have the potential to develop new innovative solutions on their own. However, internal innovation is a difficult issue and they usually need help from third parties. External assistance is generously offered by innovative fintech companies that are trying to develop new innovative products and solutions but do not have customers, which banks do. All this is an innovation path that the organization has to walk in order to get on the digital transformation train. Innovation competitions, hackathons, incubators, accelerators, startup as a company are words we should start getting used to…

“We are a technology company.” — Goldman Sachs CEO Lloyd Blankfein

A new business model is emerging that can accelerate the digitization of a bank and turn it into digital-enabled. At the same time, this situation opens a window for collaboration with technology companies, finteh, startups, developers, digital banks and services around the world.

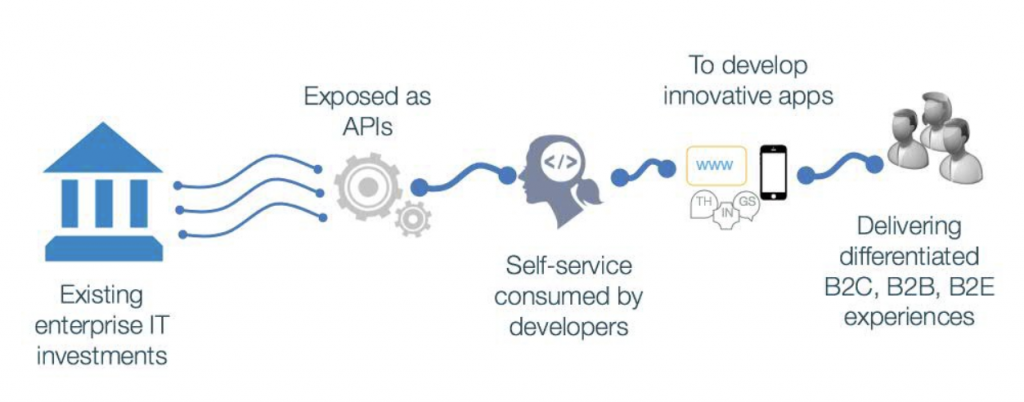

A catalyst for accelerating such partnerships is the means of communication between the bank and the new services, i.e. APIs. An API (Application Programming Interface) is the interface of the programming processes provided by an operating system, library or application to allow requests from other programs and / or data exchange.

Based on APIs, a new ecosystem of applications with multiple capabilities for those involved is created. The creation of the ecosystem leads to the cooperation of new companies, developers and technology experts with the Bank, with no geographical limitation, thus boosting and strengthening its business model internationally.

API Developers Portals are the digital meeting, documentation and collaboration space of organizations and technology providers.

Thus, their collaboration along with the help of APIs can lead to the creation of new products, applications and solutions.

Several banks have developed an API Developers portal and support the interconnection of third-party applications with their systems, thus providing new experiences to their customers.

The revised Payment Services Directive in the European Union entered into force in January 2016 and the Member States were allowed to vote on the framework by 13 January 2017.

The revolutionary change introduced by PSD2 into the European banking industry is that it “opens” the market to third-party service providers other than banks. The field of financial services has so far been subject to a particularly strict regulatory framework, as proven by the difficult conditions of entry that apply for new credit institutions.

However, the new directive provides for the authorization of third-party payment service providers. This means that innovative startup companies will be able to offer citizens unified Internet and mobile banking solutions for all banks.

For example, mobile phone apps will be connected to all the bank accounts someone has in just one app. In this way, we can conduct our banking transactions and keep up to date with our balance in other banks’ accounts with just one application.

Banks develop their own solutions internally, either by collaborating with innovative startups or by developing dedicated divisions in their structure. This is why banks hold innovation competitions – the so-called hackathons – regularly.

The digital banking market is expected to evolve in the near future.

The major change brought about by the PSD2 Directive does not only concern the regulatory framework but also the banking services model. Banks are turning from transaction banking to customer-centric banking.

Open innovation services for banks

Crowdpolicy has an integrated approach for open innovation services for Banks and the implementation of innovative applications based on the architecture of APIs.

Our approach aims to enhance the competitiveness and openness of banks, the transition to quality entrepreneurship based on innovation, full digital transition and the creation of added value with the engagement of the crowd.

The methodology we follow is based on the gradual implementation of the proposed solutions, the continuous assessment of pilot applications and the multiple repetitions until the result is achieved.

The approach of Crowdpolicy to boost innovation consists of the following:

- Creation and enhancement of various business innovation ecosystems (e.g. fintech, agrotech, civictech, insurtech, martech, IoT, health etc.)

- Creation of labs (citylabs for Municipalities) or Innolabs (for businesses) on ideation and teams development.

- Application of lean product development methodologies to develop products and services, as well as agile και scrum methodologies to develop new software products and services

- Application of lean startup methodologies to support new teams, new businesses, startups and social enterprises

- Development of social economy models

- Organization of innovation competitions Crowdhackathon

- Development of MVPs for teams, startups, businesses and organizations MakeyourMVP

- Design, support and operation of accelerators and structures for the maturation of teams and ideas

- Support of the processes by the Crowd

Bootcamps – Innovation Labs

Bootcamps are workshops during which the participants (e.g. executives of a bank, candidate teams for an accelerator etc.) are invited to solve a problem in a structured way with the use of modern development methodologies such as lean, design thinking, agile etc.

The goal is to organize the participants in groups other than those within an organization, enable them to familiarise with new technologies and ideas and learn how to work using new collaborative lean methodologies. This is the first step in order for an organization’s executives to come together and grasp modern methodologies for developing business models and products, thus promoting innovation.

During the bootcamp, the participants follow a specific way of dealing with the problem they wish to solve. Based on criteria such as human needs, a technologically feasible implementation and business sustainability, they find out what features and attributes their product or service should have in order to deal with the problem in an efficient and effective way.

Bootcamps are addressed to executives from private and public organizations as a first step towards enabling the organization’s strategy to be more agile, thus aiming at promoting innovation and effectiveness through sustainable models.

Innovation marathons Crowdhackathon

Crowdpolicy organizes the innovation competitions Crowdhackathon aiming at the creation of prototype applications and business models.

These actions are “marathons for the development of applications” on various sectors of the economy. The marathons are attended by young people, developers, designers, analysts and anyone who has ideas and suggestions to address practical problems or create a pilot innovative product or service while public and private sector bodies are engaged by providing the participants with open data.

During a crowdhackathon, the participants discuss ideas to be implemented with special mentors involved in the process. The proposals are evaluated and the most popular ones are selected to be implemented as web and smartphone applications that can be further developed. The applications that result from the competition are available as opensource so that they can be used by any interested individual or public body.

The crowd plays a vital role in all the processes of the marathon; this is why it is called crowdhackathon.

Each crowdhackathon has a leader partner that is experienced and has a great deal of knowledge on the hackaton topic We define the strategic goals on which we will work and we shape the technical specifications of the issues we wish to address in collaboration with the leader partner and the sponsors that support every crowdhackathon. A public consultation is held to co-shape the specifications of the crowdhackathon.

Participation is free for everyone.

The expenses of the crowdhackathons and the prizes awarded to the winners are provided by the sponsors, while the supporters undertake the dissemination of the action. Every time, remarkable cash prizes are awarded, about €10,000 to the first 3 winners, and sponsors provide the winners with advisory services to support business schemes, postgraduate scholarships etc.

Crowdhackathons are pleasant, we offer food and soft drinks, and at the end of the competition there is a party. You can find more information at www.crowdhackathon.com .

NBG i-bank #fintech crowdhackathon

- NBG i-bank #fintech crowdhackathon site: www.crowdhackathon.com/fintech

- Workshop Be Finnovative!: https://goo.gl/2vhpmU

- Facebook album: https://goo.gl/gxiz4O

- Video of the competition: https://goo.gl/Tl0YRy

- Github of the applications: https://github.com/NBG-i-Bank-fintech-crowdhackathon

- Blog Post: goo.gl/Fc2QTM

BoC hackathon #fintech

Bank of Cyprus held the 1st marathon for the development of applications around innovative technologies in the field of Fintech on 9, 10 and 11 June 2017 at Bank of Cyprus Cultural Foundation in Nicosia.

NGB i-bank #fintech 2 crowdhackathon

The second marathon for the development of applications in the field of Fintech NBG i-bank #fintech 2 crowdhackathon was held on 20, 21 and 22 October.

NBG i-bank #fintech 2 crowdhackathonwas was held by National Bank of Greece, with the support of Crowdpolicy, within the framework of the Bank’s broader strategy of developing partnerships with new, innovative and creative companies and teams in the field of fintech.

- NBG i-bank #fintech site: http://crowdhackathon.com/fintech2/

- Videos and Photos: https: //www.facebook.com/events/247459649088042/

Hubs of innovation and entrepreneurship

The Hub of Innovation is an initiative that promotes innovation and sustainable development. It consists of a venue where actions take place so as to support those involved.

The goal of the hub of innovation and entrepreneurship is to develop innovative business ideas and transform them into profitable outward-looking businesses. At the same time, it enables the development of the ecosystem of youth entrepreneurship through various actions so that young people will be encouraged to acquire skills and develop ideas that can transform into new businesses.

Nowadays, technologies and economic systems are evolving, and opportunities are constantly being created for the development of new innovative businesses. Through teamwork young people keep up to date with new trends and develop ideas which are transformed into commercial models and new businesses through dedicated actions.

The approach of Crowpolidcy aims at:

- Creating an innovation ecosystem for young people through the creation of an active network of innovation and entrepreneurship, which results in the creation of appropriate conditions for the continuity and sustainability of the program

- Promoting ideas, applications, teams and startups, which could result in the creation of innovative products and services that can be commercially exploited

- Networking and interacting with the market and demand

The hub brings together new businesses, young people with ideas and vision, businesses, experienced business executives, and networks the market with fresh and innovative ideas. This interaction benefits everyone. New ideas can be developed leading to the creation of new products, businesses and jobs. Moreover, the executives acquire know-how in new technologies and methodologies, the exploitation and optimal management of modern technology trends such as Internet of Things, Open Data, API Economy are promoted, and businesses can take advantage of these products for their operation or the solutions they provide to their customers.

Some of the most successful projects of Crowdpolicy are Innovathens – the Hub of Innovation and Entrepreneurship of the City of Athens, ΕΠΙΝΟΩ – the Hub of Innovation of the National Technical University of Athens, as well as be finnovative – the business accelerator of the National Bank of Greece.

Business Accelerators

Business Accelerators aim to support groups (within an organization or not) so that they can develop their MVP and to prepare them so that they can transform into sustainable businesses.

Depending on the model, a business acceleration program can be addressed to students, professionals, business executives, and anyone wishing to develop their idea or methodology and transform it into a sustainable business model. The participating teams should develop their idea in the broader thematic area of the accelerator, such as fintech, tourism, rural economy, insurance, transport, energy, shipping and so on.

The program provides participants with specialized business and technology consultancy by experienced executives, bootcamps for developing special skills, improving ideas with the use of lean development methodologies, developing MVPs and prototypes, and collaborating with mentors, businesses and accelerators from abroad.

Usually, each cycle lasts six (6) months and 5 to 15 groups are allowed to participate per cycle. The main objectives of the accelerator are the following:

- the technical and operational support of the development of applications,

- the maturation of MVPs (Minimum Viable Products) and creation of end products,

- the strategic use of data and APIs,

- the creation of a community and ecosystem,

- the exploitation of the results of competitions and innovation marathons,

- the maturation of business ventures so that they can be eligible for seed funding.

Accelerators can run within businesses so that they can support groups and synergies with the dynamic ecosystem of startups.

Community Activation

Community Activation aims to enable the startup business ecosystem to use the banking API in order for applications to be implemented by third parties.

The banking API can be used to implement systems and applications by third parties such as:

- Companies that are already producing applications and software solutions

- Individual developers

- Startups

- Fintechs

- Other,

to complete their solutions and incorporate functionalities that can be implemented using the API.

Such solutions can be addressed to end users (C) or business customers (B) and cover a wide range of applications such as:

- Mobile phone applications for payments, money transfers (mobile banking, PFM) etc.

- Automated transactions with smart assistants (bots)

- Payment systems and digital POS

- Smart applications for investments and wealth management

- Cryptocurrencies

- Retail and peer2peer loans

- Crowdfunding

- Wallets / blockchain wallets

- Special applications for Municipalities, Public sector, Agriculture, Shipping, Energy, Health, Insurance etc

This approach aims to develop initiatives to make the ecosystem aware of the Bank’s APIs, work with the Developers Portal and Sandbox, see examples of applications and build its own applications using the APIs of the Bank.

Community activation can run in addition to the strategy of implementation of the Bank’s productive APIs, as it creates the necessary interest and engagement to the ecosystem in order to attract applications to the API app marketplace and use APIs from more and more applications.

In summary, the benefits generated by community activation are as follows:

- Creation of a communication channel and cooperation with the ecosystem

- Support and continuous engagement with the community

- Technological improvement of the API based on community feedback and requirements

- Contribution to the technological upgrade of the API based on the internal API Roadmap and upgrade of the infrastructure of API Developers Portal.

Applications and IT systems

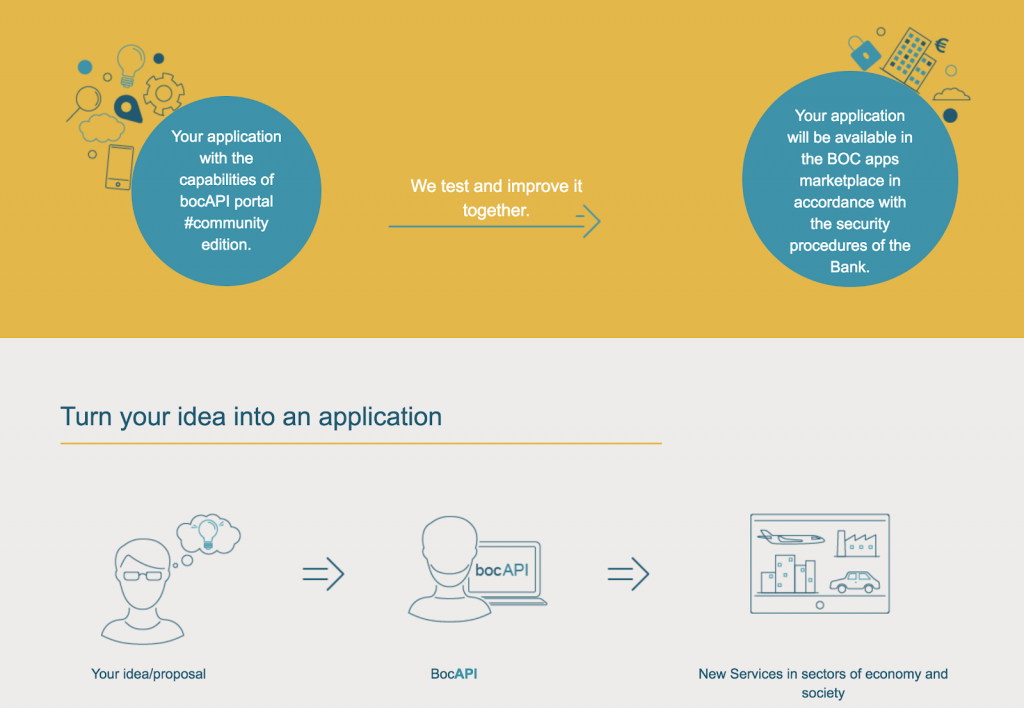

API Developers Portal

Crowdpolicy can implement the strategy for API Developers Portal to simulate or implement productive APIs based on the Open Banking standard and APIs required for PSD2.

The goal of the approach is the visual and functional integration of the Bank’s productive and Sandbox APIs with the support of value-added community activation services as well as the maturation of an API strategy.

The design of the environment aims to achieve the following:

- A direct answer on behalf of the Bank to the questions and demands of the community and those interested in experimenting or using the productive APIs

- The creation of a new service – infrastructure of the Bank for the business ecosystem, startups and developers.

- Bank innovation with technological implementations of infrastructures for the business ecosystem around fintech in the context of the broader trends around API economy

- The overall approach for the project implementation can support the maturation of necessary actions and PSD2 planning strategy

- The maturation of an API Strategy along with the additional goal of creating an ecosystem and the future implementation of an app – fintech marketplace

- Maturation of the strategic implementation of productive – legacy APIs

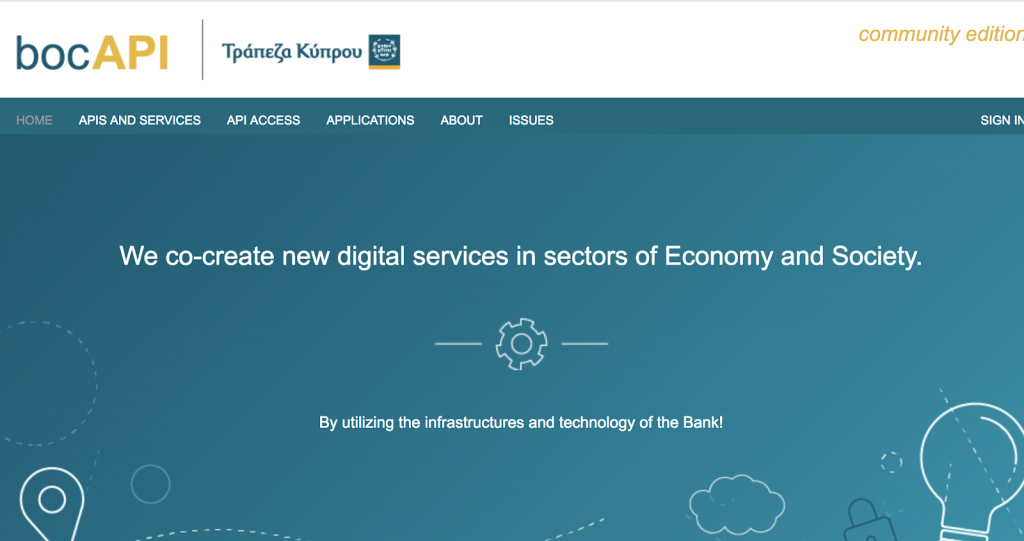

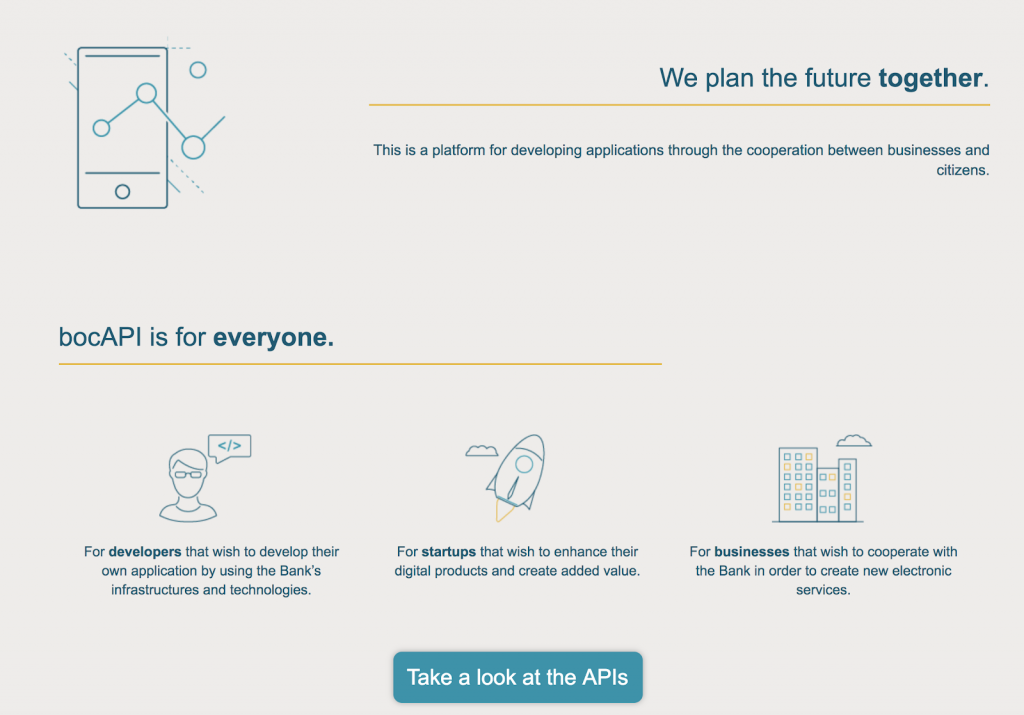

Our company has developed the API Developers Portal of Bank of Cyprus.

Implementation features:

- Node js

- Mongo DB

- Development of 5 endpoints based on PSD2

- Oauth API

- Transfer – payment API

API Developers Portal was used by 140 developers and it was also used during the boc hackathon of Bank of Cyprus.

Link: http://www.bocapi.net

Donation Crowdfunding Platform

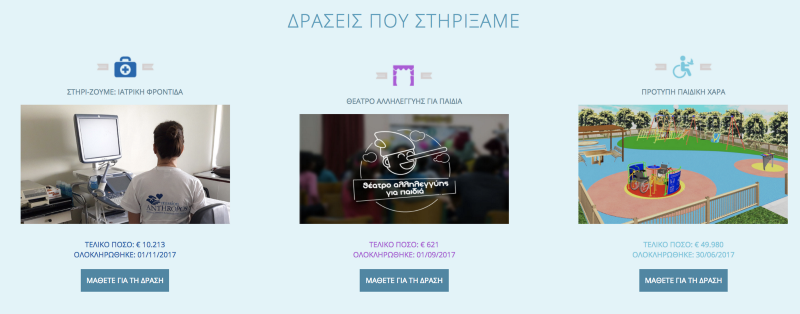

Crowdpolicy designed and implemented the IT system donation crowdfunding act4Greece for the National Bank of Greece (www.act4greece.gr).

Act4greece is an innovative program created on the initiative of the National Bank of Greece to promote significant projects needed by the Greek society and operates with the strategic cooperation of various bodies and institutions in accordance with the model of participatory financing “crowdfunding”.

It aims to raise awareness and encourage ordinary people, companies or NGOs to contribute, depending on their financial capabilities, in order to support actions with a predetermined target amount and duration.

Since February 2016, act4greece has supported 17 social actions, managed to raise more than € 1.7 million by bringing together ordinary citizens and businesses from Greece and abroad.

Crowdpolicy participated in the design and implementation of the program and the digital platform www.act4greece.gr and supports its operation.

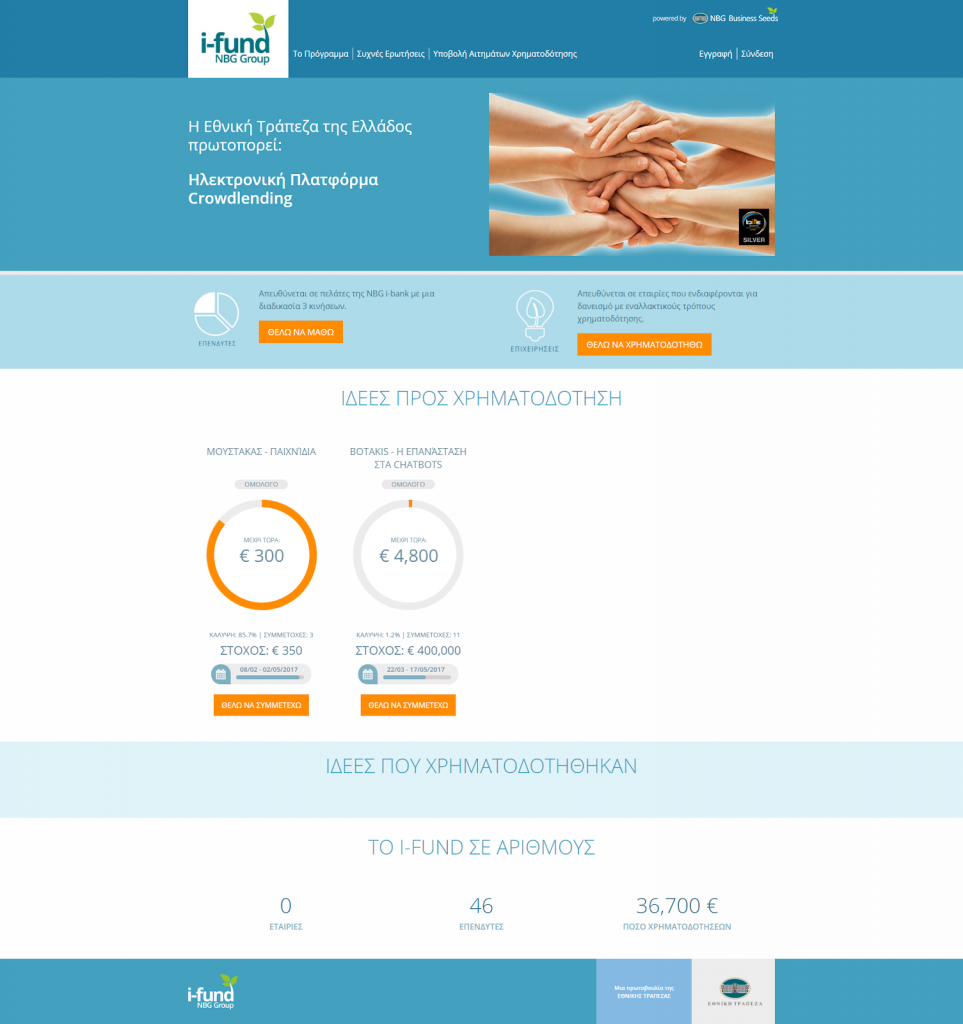

Investment Crowdfunding i-fund Platform

The platform i-fund is the Investment Crowdfunding platform of National Bank of Greece that was implemented by Crowdpolicy. The platform is connected to the systems of the Bank through APIs (accounts, investment platform etc.).

Authentication of users, oAuth, connection with eIDAS

Know Your Customer (KYC) processes of banks can facilitate authentication of citizens to log in to other private or public systems. Such a system allows citizens who already have access codes to electronic services of a bank to obtain, without additional procedures, access to specific public or private websites that have incorporated that functionality.

Similar mechanisms are now widely used, allowing users to connect to a website without having to sign up to it specifically, but alternatively use the access details they already have for another service such as Facebook, Twitter, Google Account, OpenID and in Greece via taxisnet as well.

As a result, those who have access codes to the online banking platform of their choice will be able to use them to have access as fully certified users to the online service of their choice easily and by bypassing the time-consuming steps of the initial registration – which are the ones that act as a deterrent for using a service.

This is highly beneficial, since the eGovernment services of the State become accessible to those who are currently registered to an e-banking service.

Electronic identification (eID) and Electronic Trust Services (ETS) are of vital importance to secure cross-border electronic transactions and are key structural components of the Digital Single Market.

The EU Regulation 910/2014 on electronic identification and trust services for electronic transactions in the internal market (Regulation eIDAS), adopted on 23 July 2014, is a milestone in providing a regulatory environment to enable secure and seamless electronic interaction between businesses, citizens and public authorities.

The Regulation eIDAS will increase the effectiveness of public and private services on the Internet, eBusinesses and e-commerce in the EU.

eID (electronic identification) and eTS (electronic Trust Services), electronic seals, electronic delivery service, electronic signatures etc. are inextricably linked to the requirements that are necessary to ensure legal certainty, trust and the security of electronic transactions.

In this context, the Regulation eIDAS:

- ensures that individuals and businesses can use their own national electronic identification systems (electronic identities) to access public services in other EU countries as well where the use of electronic identities is available

- creates a European internal market for eTS, ensuring they will work across borders and have the same legal status as traditional paper-based processes

Only by providing certainty about the legitimacy of all these services will it be ensured that businesses and citizens use digital interactions as a natural way of interacting.

Crowdpolicy has implemented projects on user authentication and implements the interconnection of IT systems with national eIDAS (Transofmation of Greek e-Gov Services to Eidas Crossborder Services) for national agencies.